Financial professionals have a warning for their employers: Don't ask me to come in to the office more often, or I’ll quit.

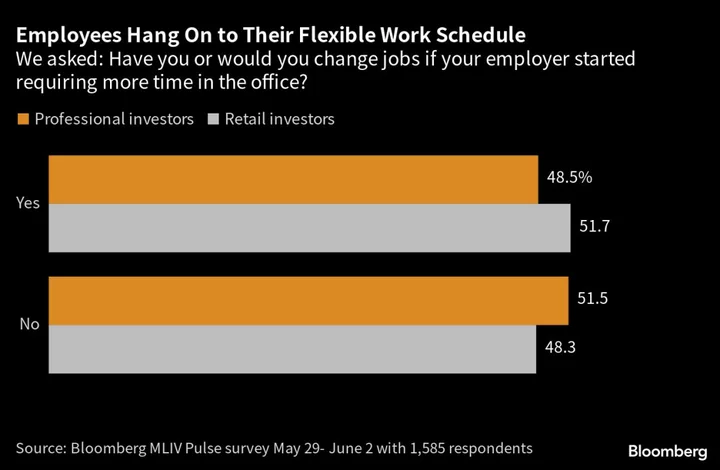

That's according to the latest Markets Live Pulse survey, which found that roughly one in two people who work in finance would change jobs — or already have — if their managers required them to spend more time in the office. More than half of the 1,585 respondents globally, which included 1,320 financial professionals and 265 retail investors, prefer a hybrid arrangement, while only about 20% favor working from the office.

The number of people responding to the survey was well above the average participants in recent MLIV Pulse surveys in a sign that return to the office is still top of mind for many professionals. Of course, pledging to quit over hybrid work is easier said under the veil of anonymity than followed through with actions.

Wall Street chiefs have been among the loudest in pushing for a return to the office five days a week. JPMorgan Chase & Co. ended remote arrangements for its managing directors in April, saying they now must be in the office every weekday. The policy comes on the heels of comments from the bank’s Chief Executive Officer Jamie Dimon earlier this year that working from home “doesn’t work” for younger staff or bosses.

About 40% of financial professionals say they already work from the office four days a week or more, according to the MLIV Pulse survey — roughly double the number that said they prefer working from the office.

Though the financial sector hasn’t seen layoffs at the same scale as tech or retail, a report from Challenger, Gray & Christmas Inc., an executive coaching firm, shows that the industry has cut nearly 37,000 jobs in the US so far this year, a figure up 320% from the same period last year. Goldman Sachs Group Inc. is working on what would be the third round of layoffs in less than a year as deal-making remains sluggish. Morgan Stanley has embarked on its second round of cuts in less than six months.

Despite these high-profile layoffs, Andy Challenger, senior vice president at Challenger, says the picture for job-hunting banking professionals isn’t as dire as it might seem. US employers added some 339,000 jobs in May, a payroll boom that far outstripped expectations and reinforced the perception that workers’ economic position remains relatively strong.

“When we look at the overall labor market, and we look at finance, unemployment remains really low, historically low,” Challenger said. “There still are job opportunities available and companies are still hiring. So it's not an awful job market to go out and look in.”

According to the MLIV Pulse poll, layoffs haven’t influenced how often people have come into the office. Only about one in 10 Wall Street professionals said the recent downsizing has motivated them to badge in more frequently.

What would be more difficult would be to find another job in the sector that has a more flexible schedule, Challenger said, as many of the big financial firms change work-from-home policies in lockstep. Still, more than two-thirds of banks offer either full flexibility or a structured hybrid arrangement, according to a survey by Scoop Technologies Inc., a firm that helps companies coordinate hybrid teams.

Moving from requiring two days in the office to three may give rise to some grumbling but likely wouldn’t be a “walk-away point,” said Rob Sadow, co-founder and CEO of Scoop. But when trying to cross the four-day threshold, employers may start to see the dynamic change.

“Four days a week or more, a lot of people will pick their head up and at least look around and see what their options are,” even if a rocky macroeconomic environment ultimately steers them to stay put, he said.

“Employees are really nervous to give even a fingernail on flexibility. Because they think if they give an inch, the employer might keep pulling,” Sadow said of the number of survey respondents who said they’d quit if asked to come in more. “So you might see really strong rhetoric or response on flexibility because they think it's not just that they're going to be asked to come in a day more — it feels like a gateway to being asked to come in full time.”

For now, the most powerful determinant of how much time people spend in the office appears to be company policies: About 86% of financial professionals are complying with their company’s in-office mandates. Those that aren’t meeting the requirements say that most of the time, they’ve faced no consequences. Of the 1,320 financial professionals surveyed, only 28 said they’ve been reprimanded by their manager or HR for failing to comply. Five respondents said they’d faced compensation-related penalties and two said they’d faced termination.

City leaders have been among the most outspoken in calling workers back to the office, concerned about the impact remote work has had on their downtowns. New York City, for example, is losing more than $12 billion a year as workers spend 30% fewer days in the office and therefore give less business to Manhattan vendors during the week, according to a Bloomberg News analysis. New York, along with Chicago, San Francisco and Philadelphia, are still seeing a deep decline in weekday lunch traffic compared to before the pandemic, according to the restaurant management software provider Toast — a trend attributable both to hybrid work and to inflation bringing up the cost of eating out.

MLIV Pulse survey showed that even financial professionals, who typically have more disposable income than the average city resident, are reigning in their weekday spending: While half reported that their dining habits post-pandemic haven’t changed at all, about a third are packing their lunch, eating office food or going straight home without grabbing after-work drinks more often than they used to.

MLIV Pulse is a weekly survey of Bloomberg News readers on the terminal and online, conducted by Bloomberg’s Markets Live team, which also runs a 24/7 MLIV Blog on the terminal. The survey about return to office, conducted May 29- June 2, drew responses from portfolio managers, researchers, strategists, economists, traders, investment bankers, as well as retail investors.

This week, the survey focuses on prices, profit margins and power. Do you feel some corporations raised prices more than they needed to to beef up their margins? Share your views here.